Posted in Uncategorized | Leave a Comment »

U.S. VC Deal Flow Slides for Three Quarters for First Time Since 2009

SHARE:

Click to see more

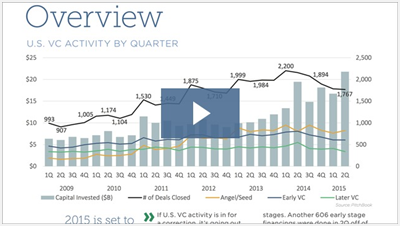

PitchBook’s 2H 2015 VC Valuations & Trends Report unveils the hottest trends within the venture capital industry, taking a deep dive into a decade of VC valuations, financings and series terms. To summarize the key findings, we’ve produced a short video, which highlights some particularly interesting details regarding today’s venture industry, including:

$21.8 billion was invested in 2Q 2015, another post-crisis record. Despite this, deal flow has steadily decreased since 1Q 2014.

Median Series A and B valuations have increased to $15.1M and $41.4M, respectively. Median Series D+ valuations are at an all-time high ($184M).

32 startups entered the realm of unicorns through August of this year. This number nearly eclipses last year’s record high of 33.

Click here to download the full report for free, click here.

Posted in Uncategorized | Tagged PitchBook Newsletter, Private Equity, VC Deal flow, Venture Capital | Leave a Comment »

Key Takeaways for Venture Capitalists Working with Troubled Companies

By Thomas Hwang and Darryn Beckstrom

Venture capitalists (“VCs”) often provide needed debt financing such as bridge loans to emerging companies in financial distress. However, given their insider status with these companies, VCs may encounter issues with such financing in the event the emerging company files for relief under the Bankruptcy Code. One issue arises in the context of the potential conflict with the goal in bankruptcy to ensure that claims against a debtor’s estate are administered in an equitable fashion. Among other things, bankruptcy courts will seek to preclude lenders from disguising equity investments or capital contributions as loans in order to obtain the same priority treatment with a company’s creditors in the event their investments fail and the company commences a bankruptcy case. In bankruptcy, parties may request that the court invoke its equitable powers under theories of equitable subordination and debt recharacterization, effectively to subordinate a VCs’ claim in bankruptcy arising from such financing.

For these reasons, as discussed further below, VCs should always be mindful of the terms of and negotiations surrounding transactions they enter into with emerging companies as well as their ongoing interactions with these companies.

Equitable Subordination

A bankruptcy court has the power under section 510(c) of the Bankruptcy Code to equitably subordinate an allowed claim to other claims. Section 510(c) does not set forth the requirements for equitable subordination. But the majority of courts have held that a claim may be equitably subordinated under the following circumstances: (1) the claimant engaged in some type of inequitable conduct; (2) the misconduct resulted in injury to the creditors of the bankrupt or conferred an unfair advantage on the claimant; and (3) equitable subordination of the claim is not inconsistent with the provisions of the Bankruptcy Code. Courts have concluded that inequitable conduct usually involves the following types of behavior by the claimant: (1) fraud, illegality, and breach of fiduciary duty; (2) undercapitalization; and (3) use of the debtor as a mere instrumentality or alter ego. Under the requirements for equitable subordination, a court focuses on the behavior of the claimant whose claim a party seeks to have subordinated rather than the substance of any particular transaction.

Under equitable subordination, a court may scrutinize claims held by insiders, such as VCs, more carefully than those held by non-insiders. Specifically, a court may equitably subordinate a claim if the party seeking subordination can simply demonstrate some inequitable conduct on the part of the claimant and the claimant should be held responsible for such behavior. Conversely, parties seeking subordination will need to demonstrate that a non‑insider claimant engaged in more egregious behavior, such as fraud, before a court will consider subordinating a claim.

If the elements of equitable subordination are satisfied, a court will subordinate the claim only to the extent necessary to offset any injury or damage suffered by the creditor that suffered as a result of the claimant’s inequitable conduct.

Debt Recharacterization

Alternatively, a bankruptcy court may use its equitable powers under section 105 of the Bankruptcy Code to recharacterize any transaction the parties characterize as debt as an equity contribution to the debtor. Debt recharacterization differs from equitable subordination in that the former focuses generally on the substance of the transaction while the latter focuses solely on the behavior of the claimant. Further, when a claim is equitably subordinated, it is still considered debt of the debtor. But when a claim is recharacterized, the alleged debt is considered equity. Compared to equitable subordination, this remedy is especially problematic for VCs because it does not require a finding of inequitable conduct. Instead, the court must simply determine whether a debt actually existed or whether the alleged debt is disguised as an equity contribution. If the claim is recharacterized, then it is subordinated to the level of equity.

Courts within all federal circuits have permitted debt recharacterization, and there has been no indication that application of the remedy is restricted to shareholder loans. In so doing, the majority has applied a flexible factor test articulated by the Sixth Circuit known as the Roth Steel/AutoStyle test, based on the bankruptcy court’s equitable powers under section 105(a) of the Bankruptcy Code, looking to such factors as: (1) the names given to the instruments, if any, evidencing indebtedness; (2) the present or absence of a fixed maturity date and schedule of payments; (3) the source of repayments; (4) the right to enforce payment of principal and interest; (5) the adequacy or inadequacy of capitalization; (6) the identity of interest between the creditor and the shareholder; (7) the security, if any, for the advances; (8) the corporation’s ability to obtain financing from outside lending institutions; (9) the extent to which the advances were subordinated to the claims of outside creditors; (10) the extent to which the advances were used to acquire capital assets; and (11) the presence or absence of a sinking fund to provide repayments. See In Roth Steel Tube Co., 800 F.2d 625, 630 (6th 1986); In re AutoStyle Plastics, Inc., 269 F.3d 726,731 (6th Cir. 2001). None of these factors are dispositive, and courts will consider all circumstances surrounding the alleged debt at issue.

While the majority of circuits will analyze the foregoing Roth Steel/AutoStyle factors in considering whether to recharacterize a debt, others have looked elsewhere. The Eleventh Circuit has employed, in some instances, a limited test focused on two circumstances: “Shareholder loans may be deemed capital contributions in one of two circumstances: where the [debtor] proves initial under-capitalization or where the [debtor] proves that the loans were made when no other disinterested lender would have extended credit.” In re N & D Props., 799 F.2d 726, 733 (11th Cir. 1986). However, courts within the Eleventh Circuit have varied employing the N & D Properties test in some cases and various multi-factor tests in others. See In re First NLC Fin. Servs., 415 B.R. 874, 880 (Bankr. S.D. Fla. 2009) (listing cases).

The Fifth and Ninth Circuits more recently have addressed the issue, declining to follow the majority and instead looking to section 502(b) of the Bankruptcy Code (pertaining to the allowance of claims) as authorization to recharacterize and holding that state law should govern the determination of the nature and scope of a right to payment unless a federal interest requires otherwise. In re Fitness Holdings Int’l, Inc., 714 F.3d 1141, 1148–49 (9th Cir. 2013); In re Lothian Oil, Inc., 650 F.3d 539, 542–44 (5th Cir. 2011).

Recently, the Tenth Circuit addressed the demarcation between jurisdictions in Redmond v. Jenkins (In re Alternate Fuels, Inc.), 2015 U.S. App. LEXIS 9915 (10th Cir. June 12, 2015), and expressly rejected the minority view, explaining that the concept of recharacterization is rooted in section 105(a) and not section 502(b) of the Bankruptcy Code:

Although related, disallowance and recharacterization require different inquiries and serve different functions. Under § 502(b), disallowance of a claim is appropriate “when the claimant has no rights vis-à-vis the bankrupt, i.e., when there is ‘no basis in fact or law’ for any recovery from the debtor.” … Recharacterization, on the other hand, is not an inquiry into the enforceability of a claim; instead, it is an inquiry into the true nature of a transaction underlying a claim. In this way, recharacterization is part of a long tradition of courts applying the “substance over form” doctrine.

Id. at *16 (internal citations omitted).

The Tenth Circuit ultimately determined that neither equitable subordination which it deemed “an extraordinary remedy to be employed by courts sparingly” nor recharacterization, after application of its own 13-factor test, were appropriate. As a policy consideration, the court refused to overemphasize the undercapitalization and financial condition of the debtor company because it would discourage lenders, including business owners, to provide rescue financing in similar situations. Notably, the court also pointed out that the promissory notes in question were not found to be invalid or unenforceable under applicable state law and that sufficient consideration was exchanged under state law. Thus, while rejecting the minority view, the Tenth Circuit’s decision still included analysis of applicable state law. While the Alternative Fuels decision appears to be favorable for lenders and business owners, it more importantly provides a reminder that the split among circuits remains and that both state law and the Roth Steel/AutoStyle factors warrant consideration.

What Should VCs Do When Dealing With Emerging Companies?

Most importantly, VCs should provide debt financing to emerging companies on terms that are consistent with arm’s-length negotiated financing provided by non‑insiders. Courts have emphasized that the more the transaction in question resembles a transaction negotiated at arm’s‑length, the more likely it will treat the transaction as debt rather than equity. Further, VCs should make sure that any debt financing provided to these companies reflect the characteristics of debt rather than equity, including the terms of the financing as well as how the transaction is documented. Notably, in some instances, courts employing both the majority and minority analyses may look to ascertain the intent of the parties. E.g., Alternative Fuels, supra, at *26; Bauer v. C.I.R., 748 F.2d 1365, 1367 (9th Cir. 1985) (applying California state law). Finally, VCs must make sure their dealings with the company on an ongoing basis reflect an upholding of the fiduciary duties they owe to the company.

Financial Restructuring requires more than just knowledge of the Bankruptcy Code. Dorsey’s Bankruptcy and Financial Restructuring group includes not only experienced bankruptcy lawyers, but also a large network of lawyers experienced in mergers and acquisitions, corporate governance, tax law, securities law, finance, business litigation, labor and employment and other disciplines that are critical to the restructuring of viable businesses and assisting creditors and others in preserving their rights. Learn more at: www.dorsey.com/financial_restructuring_bankruptcy/

Posted in Uncategorized | Tagged Darryn Beckstorm, Distressed Companies, Dorsey & Whitney, Thomas Hwang, Troubled Companies, Venture Capital | Leave a Comment »

San Francisco, September, 2015

Successful Acquisition of Medical Device Intellectual Property/Patents by Gerbsman Partners for a Coronary Vascular Medical Device Company

Steven R. Gerbsman, Principal of Gerbsman Partners, announced today his success in acquiring Intellectual Property/Patents in vascular technology for a coronary/vascular medical device company. The IP/Patents focus on an external support device for saphenous veins that is used as bypass conduits in coronary artery bypass grafting (CABG) surgery.

Gerbsman Partners provided Financial and Strategic Advisory leadership to its Client, facilitated the sale of the Intellectual Property/Patents and closing of the sale. Due to market conditions, Gerbsman Partners Client made the strategic decision to seek to acquire certain Intellectual Property/Patents. Gerbsman Partners provided leadership to the company with:

- Business Consulting and Investment Banking domain expertise in developing the strategic action plans for the strategy to acquire Intellectual Property/ Patents;

- Proven domain expertise in acquiring and Intellectual Property/Patents;

- The ability to “Manage the Process” among Acquirers, Seller, Lawyers, and Management;

- Communications with the Client’s Board of Directors, senior management, sthe seller and parties in interest.

About Gerbsman Partners

Gerbsman Partners focuses on maximizing enterprise value for stakeholders and shareholders in under-performing, under-capitalized and under-valued companies and their Intellectual Property. Since 2001, Gerbsman Partners has been involved in maximizing value for 91 Technology, Medical Device, Life Science, Solar, Fuel Cell, Cyber/Data Security and Digital Marketing companies and their Intellectual Property and has restructured/terminated over $810 million of real estate executory contracts and equipment lease/sub-debt obligations. Since inception in 1980, Gerbsman Partners has been involved in over $2.3 billion of financings, restructurings and M&A transactions.

Gerbsman Partners has offices and strategic alliances in San Francisco, Boston, New York, Washington, DC, McLean, VA, Europe and Israel.

GERBSMAN PARTNERS

Phone: +1.415.456.0628

Email: steve@gerbsmanpartners.com

Web: www.gerbsmanpartners.com

BLOG of Intellectual Capital: blog.gerbsmanpartners.com

Posted in Uncategorized | Tagged Gerbsman Partners, Intellectual Property, Medical Device, Patents, steven r gerbsman | Leave a Comment »

How to Live Independently as We Age

A care conference offers insights on elder abuse, dementia and suicide

As the US and the World is dealing with an “aging population”, insights and strategies for the “elderly”, will be/are critical for navigating all facets of life. Over the next months, Gerbsman Partners will provide updated information on this topic, along with business, family and personal strategies.

Next Avenue Blogger

Credit: Liza Kaufman Hogan

Role playing during a session on suicide prevention

This week I attended my first National Home and Community Based Services Conference, an annual gathering of professionals who provide services for older adults and disabled individuals who wish to remain in their homes and communities as they age.

More than 1,400 people are attending this year’s event, sponsored by the National Association of States United for Aging and Disabilities.

Assistant Secretary for Aging Kathy Greenlee kicked off the conference with a speech marking the 50th anniversary of Medicare, Medicaid and the Older Americans Act (OAA).

Frustration With Washington, But Progress, Too

“As advocates, we specialize in being frustrated with these programs. We know we need more funding for OAA, we know there are gaps in Medicare … and we know we need to do more balancing with Medicaid,” said Greenlee. Despite these frustrations, she exhorted the audience “to look at the foundation of support the programs have created in our country. These three programs demonstrate that we as a nation have made tremendous investments in the health and life of our citizens as they age and are disabled.”

The Older Americans Act, which has not been reauthorized since 2006, serves 11 million Americans by providing vital nutrition assistance (Meals on Wheels), help with transportation, caregiving, legal services and elder abuse prevention, as Next Avenue blogger Robert Blancato wrote earlier this year.

In solving problems for those with dementia, Mosqueda views the whole family as her patient.

The U.S. Senate acted to reauthorize the law in July, but the House has not yet taken it up for a vote. “We continue to be engaged with members of the House and staff, and we are very hopeful the House will also move soon to reauthorize this law,” Greenlee said.

Dealing with Dementia and Elder Abuse

I later attended an engaging talk on “The Risk of Abuse for Cognitively-Impaired Older Adults,” by Dr. Laura Mosqueda, director of the National Center on Elder Abuse, chair of the Family Medicine Department and the associate dean of primary care at the Keck School of Medicine at the University of Southern California.

Sharing statistics showing that Alzheimer’s and other forms of dementia are expected to grow exponentially as the American population ages, Mosqueda said: “If ever there was an epidemic that we knew was coming, this is it, and we are not prepared for it.”

Mosqueda, a practicing physician who works with patients diagnosed with a variety of dementias, outlined types of memory loss and explained how they can interfere with the reporting and redress of elder abuse. Although there is a tendency to lump all forms of dementia together, she said knowing that someone has Frontotemporal Dementia, as opposed to Alzheimer’s, allows an attentive doctor to access the parts of the memory circuit that are still working to figure out what happened.

She said it is incumbent on doctors to work with law enforcement to help them investigate charges of elder abuse where the victim may have significant memory loss. Mosqueda cited an example of a patient who could not speak well but was able to identify her caregiver and alleged abuser with photos.

MoreIt’s Time to Get Serious About Elder Abuse

She also offered tips for communicating and calming people with dementia, such as not arguing with someone who is having a delusion. One of her patients, she recalled, was certain that Gen. Norman Schwarzkopf was in her room to offer strategic war advice. As funny as that sounds, it was distressing to her patient.

Said Mosqueda: “You don’t argue with a person with delusion. It is as real to them as it is to you that it’s not (real).”

Instead, she said, you should “acknowledge and distract” by saying something like: “That must be so scary for you. I’m going to see what we can do to make sure that doesn’t happen anymore.”

This is helpful for the person with dementia, who may get agitated if his or her assumption is challenged, and also helpful in reducing stress on caregivers, which may trigger neglect or abuse, Mosqueda said.

In solving problems for those with dementia, Mosqueda said she views the whole family as her patient, so she can better understand how all members are affected by the illness and its caregiving consequences. At the center, however, is the person with dementia and his or her wishes, as much as they can be discerned. “It’s the ‘nothing about me without me’ that we have to pay attention to,” Mosqueda noted.

Suicide Prevention Among Older Adults

The last session I attended, “Preventing Suicide Among Older Adults,” highlighted new tools and programs to help caregivers and professionals identify suicide risks and respond appropriately.

According to the Suicide Prevention Resource Center (SPRC), suicides for most age groups has been rising since 2000 with the sharpest increase for people 45 to 64. Overall, men die by suicide at four times the rate of women.

MoreSuicide Risk in the Elderly

During her presentation, SPRC’s Christine Miara said the top three suicide warning signs are:

1. Talking about wanting to die or kill oneself

2. Looking for a way to kill oneself

3. Talking about feeling hopeless or having no reason to live

Some of the risk factors for suicide among older adults include:

- The death of a loved one

- Physical illness

- Uncontrollable pain or the fear of a prolonged illness

- Perceived poor health

- Social isolation and loneliness

- Major changes in social roles (such as retirement)

If someone you know is considering suicide, call 911 or the National Suicide Prevention Hotline at 800-273-TALK. If it is not an emergency and your loved one lives in a residential facility, discuss your concerns with a supervisor there.

Miara said that senior centers and residential communities, these days, are doing more to address mental health issues and adding programs to combat some of the risk factors through social and educational programs. For additional information, she recommended these fact sheets from the Substance Abuse and Mental Health Services Administration.

Posted in Uncategorized | Tagged Aging, Liza Kaufman Hogan, Next Avenue, Senior Citizens | Leave a Comment »