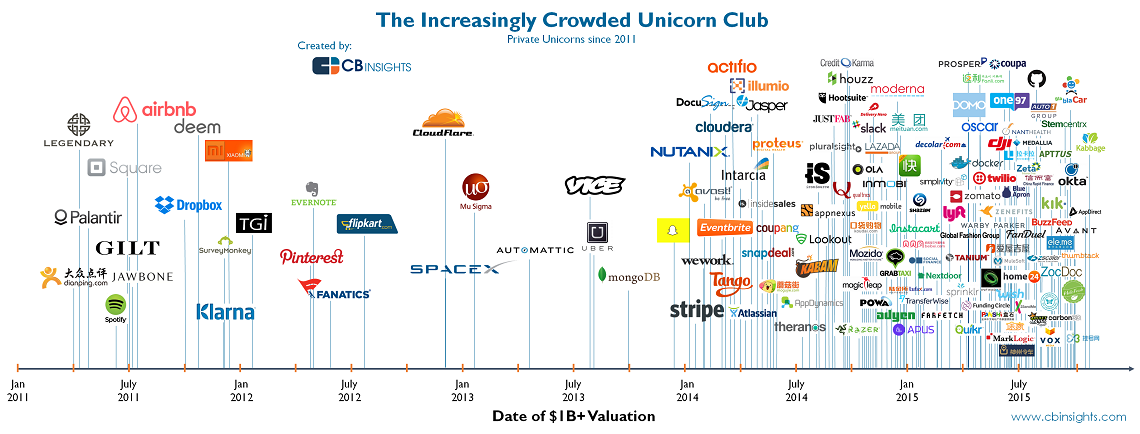

Boo: The increasingly crowded unicorn club in one infographic

In honor of Halloween, here is our scariest infographic ever. We visualize the rise of unicorn companies since 2011. So much for unicorns being mythological.

Posted in Uncategorized, tagged Anand Sanwal, CB Insights, Unicorn Club on October 31, 2015| Leave a Comment »

Boo: The increasingly crowded unicorn club in one infographic

In honor of Halloween, here is our scariest infographic ever. We visualize the rise of unicorn companies since 2011. So much for unicorns being mythological.

Posted in Uncategorized, tagged CB Insights, Global Venture Capital Report on October 17, 2015| Leave a Comment »

Global Venture Capital Report – Q3 2015 KPMG and CB Insights: VC-backed Companies Haul in US$37.6 Billion Globally in Q3 2015 Due to Mega-Rounds and Continued Crossover Investor Activity- from CB Insights

An in-depth analysis into the financing trends including unicorn growth, mega-rounds, country breakdowns, the most active investors, and more.

Posted in Uncategorized, tagged CB Insights, domains, Dotcom, Non-Dotcom Bubble on August 26, 2015| Leave a Comment »

.com is still the king of suffixes. But startups are also flocking to other domains, including .io.

In a recent essay, Paul Graham recommended that startups should own their .com domain name or risk being considered marginal or weak. However, .com domains can be very expensive, especially for younger startups. We used the CB Insights database to analyze the trends in startup domain suffixes over time, such as the rise of the .io suffix.

Traditional .com domains still dominate amongst the more than 25,000 tech companies funded since 2010, with 20,000+ companies choosing a .com domain for a 81% share of all suffixes.

But other domain suffixes are also popular. These include .net and .co domains, which proved to be the most popular, followed by .io which saw nearly 350 funded tech companies choosing that domain. After the top 3, the list is populated mostly by more geography-specific domains such as .de (Germany), .cn (China), and .jp (Japan). Also, .tv has been used by more than 100 companies, including well-known services Twitch.tv, blip.tv, and acfun.tv. The .ly domain, often considered a go-to suffix for Silicon Valley startups, isn’t really all that popular.

With a flurry of new domains having been made available by ICANN recently starting in 2014, startups will increasingly seize the opportunity and flock to alternative domain suffixes. But many of the newest suffixes like .global are not showing up on the radar just yet.

Among the top URLs, some have seen more growth than others in recent years.

The number of unique domain suffixes attached to startups in a given year saw a significant jump between 2011 and 2012. There were 116 separate domain suffixes used by startups this year through mid-August 2015, almost double the amount in full-year 2010.

It’s not uncommon to see new domain suffixes pop up when looking at startups receiving funding (i.e., suffixes that have never been attached to a tech startup before). Below are select new domain suffixes that have been funded recently as well as the companies attached to them. In 2015, we saw new startups with .soy and .world suffixes. Some are country-level geographic suffixes, e.g. .dj is Djibouti.

| Select Newly Funded Domain Suffixes | ||

| Year | Suffix | Select Companies |

| 2012 | .global, .om, .gg, .pro | bluedot.global, pinion.gg, bad.gy, cpac.pro |

| 2013 | .dj, .ae, .bi, .sr | plug.dj, propertyfinder.ae, bbs.bi, hairdres.sr |

| 2014 | .limo, .life, .works, .today | loup.limo, league.life, weave.works, celuv.today |

| 2015 YTD | .ventures, .world, .soy, .pictures | entangled.ventures, myeye.world, bevisible.soy, folio.pictures |

Posted in Uncategorized, tagged Anand Sanal, CB Insights, e-Commerce on July 21, 2015| Leave a Comment »

We’ll make it up in volume

Hi there,

Ever wonder which VCs are the best at spotting unicorn companies earliest? Wonder no more. See who the unicorn whisperers are below.

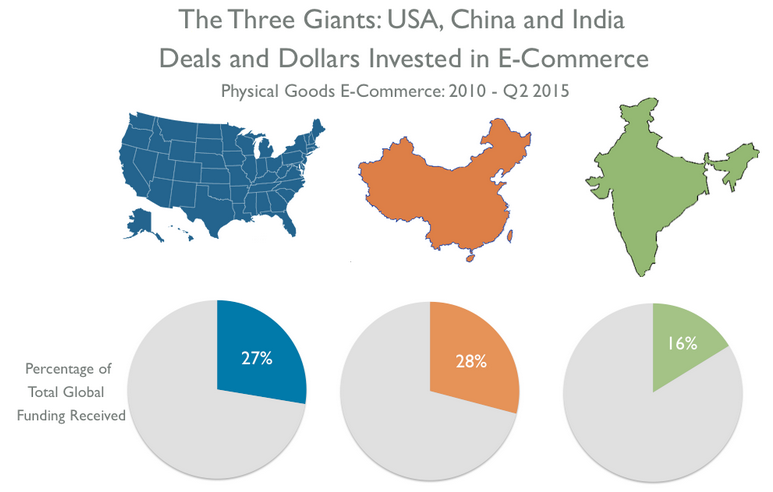

e-Commerce’s big three

When it comes to eCommerce investment, it’s China, India, the US and then everyone else. The 3 markets account for 62% of global deal activity and 71% of total funding.

Speaking of e-Commerce – this will be interesting

Jet.com, the startup founded by Diapers.com alumni Marc Lore, launched today and although it projects big losses and competition from Amazon, it is also rumored to be in talks to raise financing at a valuation of 3 unicorns.

So we wanted to anonymously ask you and 88,000 of our closest friends what you think of Jet’s prospects. Simply click below and we’ll report the results in the next newsletter.

Will Jet.com live upto the hype and become a credible competitor to Amazon?

lowest 1 2 3 4 5 6 7 8 9 10 highest

Google Ventures is slowing down

For our corporate VC benchmarking webinar next week, we’ve been digging into the performance of several notable corporate VCs. Today, we refreshed our Google Ventures teardown and see the CVC arm of Google is slowing down their investment pace while exits have ticked up as the company’s portfolio matures. More graphs and charts about their industry and geographic strategy than you’ll know what to do with.

Quotable & Notable

We’re the most trusted source for VC and startup data by the media (seriously).

And it’s always good to see how our data intersects with larger stories our media friends are working on. Here are a couple that recently caught our eye.

Connie Loizos of TechCrunch highlights how startup employees are wising up.

“This week, a Bay Area founder was taken aback when an engineer being recruited by his startup asked for both its cap table and information regarding the liquidation preferences of its venture backers.”

Bloomberg’s Adam Satariano & Jing Cao discuss how fear is trumping greed for Valley VCs.

“While Silicon Valley heatedly debates whether technology valuations have risen to excessive levels, the investors who helped fuel the boom aren’t waiting for an answer. Venture capital firms are starting to take steps to protect themselves in the event of a downturn.”

Paul Mozur of The New York Times digs into Asia’s startup boom.

“Across Asia, investments in technology start-ups have escalated at the same swift pace and to the same heights as in the United States.”

Sarah Lacy of Pando says we need to stop talking about the sharing economy.

“Without Uber, the sharing economy would be an economy like Greece is an economy. You only have to look at the numbers to realize just how much the rest of the so-called “sharing economy” is left– comparatively– in the dust.”

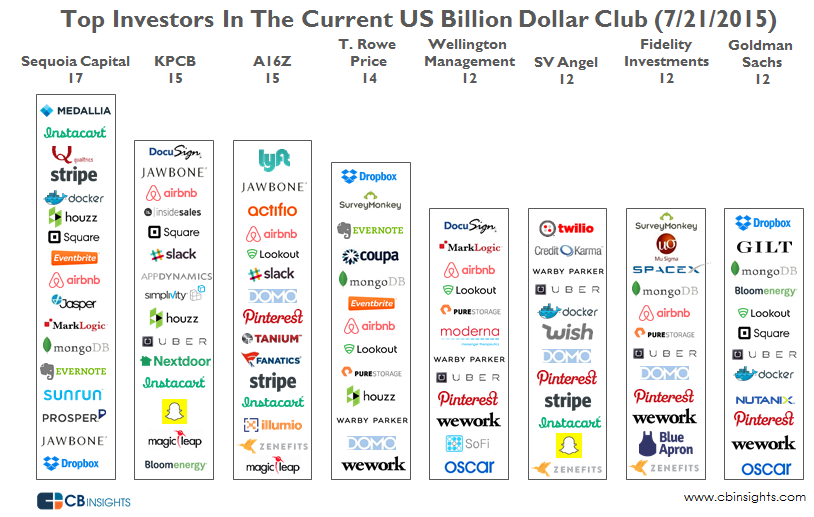

The unicorn whisperers

Which investors are in the most unicorn companies and more importantly, which investors got into these companies earliest? Your daily dose of unicorn data is here.